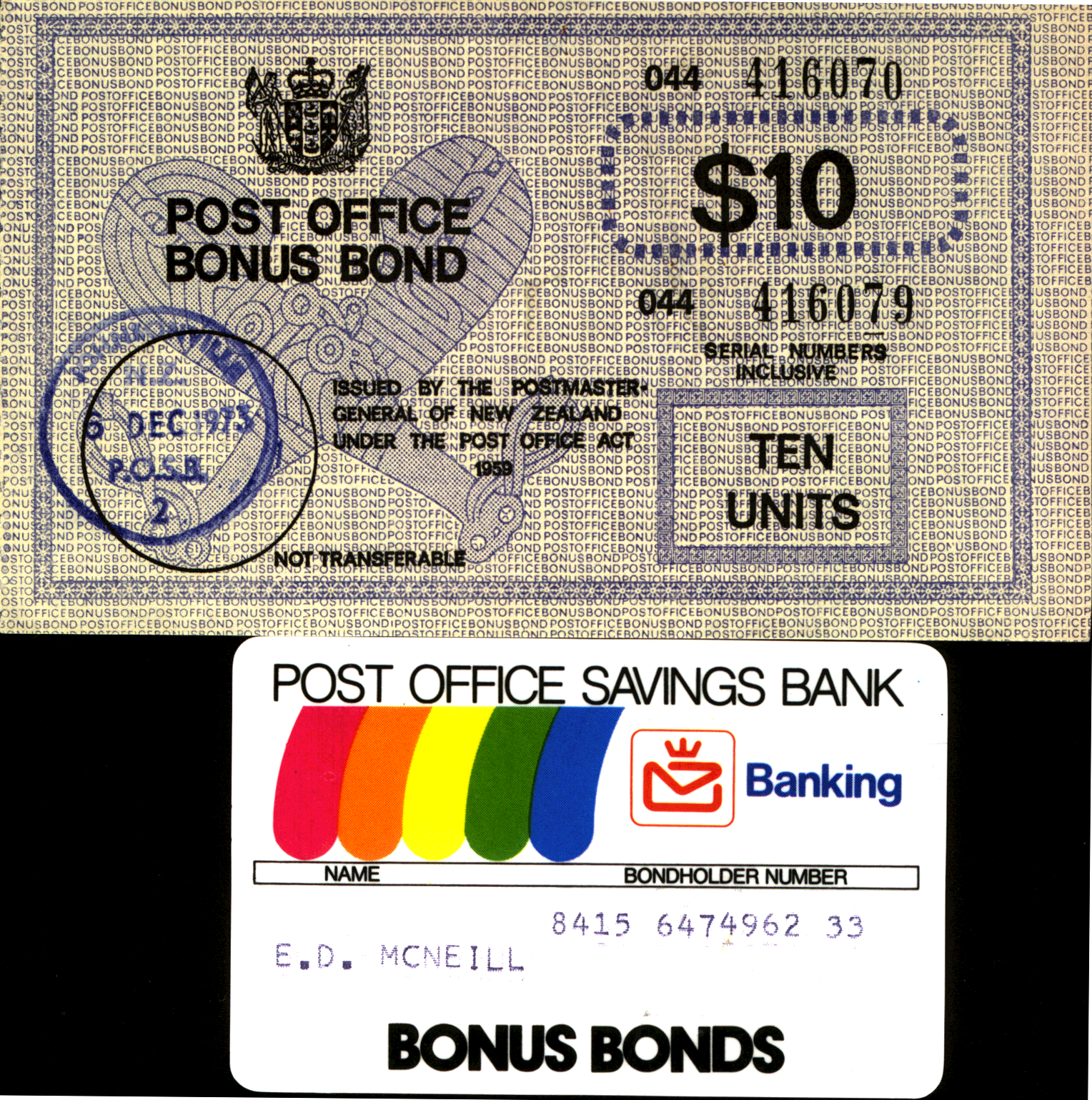

On 6 December 1973, shortly after my birth, my parents bought 10 Post Office Savings Bank Bonus Bonds for me, for a cost of $10. (These are 044-41670 to 044-416079.) As far as I'm aware this Bonus Bonds scheme got transferred through various bank mergers so that 36 years later it is part of the ANZ National Bank, and I believe the obligations transferred with each merger, including the change to a unit trust structure about 20 years ago.

The Bonus Bonds scheme started in 1970, based on an investment trust paying no interest but with a "chance to win" every month. In theory they notify everyone who wins regardless of the size of the prize, so in theory if I had ever won anything I would have been notified. (My parents have not moved in my lifetime and presumably gave their address at the time of purchase.) If I did win something and somehow didn't get notified, then the prize would be reinvested.

The Bonus Bonds have a monthly draw, near the start of each month, and bonds are eligible for the draw after they've been owned for at least a full calendar month (which I'd guess was done to avoid people gaming the system by buying at the end of the previous month and redeeming after the draw). So for my bonds the first draw they would have been eligible for would have been the February 2004 draw and the most recent draw is the November 2009 draw, making for two years with 11 draws, and 34 full years in between. That makes for a total of 430 draws ((2 * 11) + (34 * 12).

Apparently there is between a 1/9600 and 1/16000 chance of winning each month, per bond, at present (it's presumably changed a bit over time. Taking the average of those two, that's in the order of a 1/12500 chance of winning (wikipedia lists a 1/11000 chance of winning at present, presumably based on older information). For 430 draws, with 10 bonds, that works out to a combined total of a 29.11% chance of ever having won anything at all (29.11% == (1-((1-(10/12500))430))*100; viz, calculate chance of always losing, then invert that, assuming 10 chances to win each month due to having 10 bonds). Supposedly the average prize is $27.51 in a good month, and presumably lower in other months.

So basically like a lotto ticket, but with the advantage of "retaining" the capital. Unfortunately inflation has somewhat reduced the value of the original $10 outlay, as shown by the Reserve Bank Inflation Calculator. $10 in the fourth quarter of 1973 would have bought approximately the same quantity of goods as $100 buys now, for a 90% decline in purchasing power. Inflation is a harsh mistress, given 36 years to work. In contrast to "holding cash without interest" gold was a rather better investment over those 36 years, climbing from approxiately US$140/ounce (1975) to US$865/ounce (2008), for an increase in value of around 6 times -- which still represents a substantial reduction in purchasing power. (Depending on what happened beween 1970 and 1974, the actual increase in value might be slightly higher, but still seems to be a net loss in real value.) Something in the order of 6-7% interest, after tax, would have been required to retain the purchasing power over that 36 years -- which may have been achievable as interest rates definitely spiked in the 1980s, and even in the last couple of years interest rates have been over that.

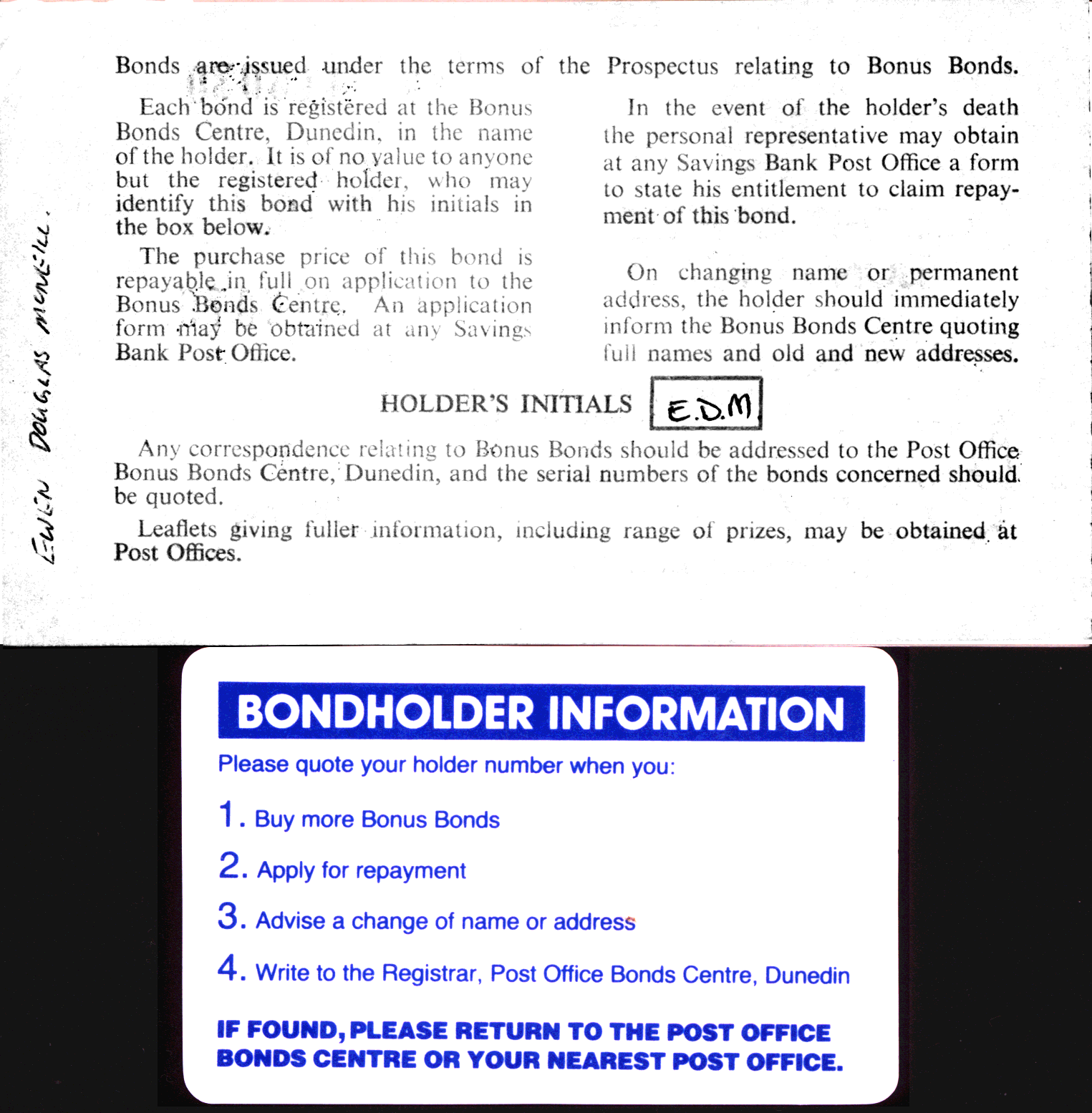

According to the bond certificate that I have, "The purchase price of this bond is repayable in full on application to the Bonus Bonds Centre. An application form may be obtained at any Savings Bank Post Office.". These days they appear to be redeemable by application at an ANZ Bank branch, but appear to no longer guarantee face value redemption stating that it depends on how well their investments did (presumably not exactly brilliantly in the last year or so...). It takes 5-28 days to receive the money back unless you request an emergency redemption which costs $60 (so defintely not worth it for my $10!). None the less it seems the best action is to redeem the 10 Bonus Bonds as soon as possible to salvage the 10% of value still left -- it might even buy lunch the day it is refunded.

Interestingly the Bonus Bonds scheme is not covered by the Government Guarantee, but is apparently rated "AAAf" by Standard And Poors (the "f" subscript indicates a fund rating). Of course since these are the same agencies that gave AAA ratings on subprime mortgage backed securities that means rather less than it used to mean. (I was amused to see a week or so back one of the NZ finance companies offering a remarkably high interest rate proudly advertising their "BBB+" rating -- considering what was being given "AAA" ratings in the past few years, one wonders just what bad shape one needs to be in to get a "BBB"-type rating....)

ETA: Checking my Bonus Bonds turned out to be as simple as going to a teller at my local ANZ branch and giving them the card with my bond holder numbers. Their computer system still recognised it, and confirmed that I'd never won anything. Refunding it required the teller filling out a form (which they had a pile at the teller desk) to request it to be refunded into a bank account. Apparently it will take a week. (front back)

{kind=link}

{kind=link}

ETA 2: The refund arrived in my account by Tuesday morning, even less than the week predicted. Now to decide what to do with my new found "wealth".

ETA 2010-01-14: I had a phone call from a reporter at The Herald who was doing a story about the 40th anniversary of Bonus Bonds. He did a brief phone interview, and said he'd email me when the story had been published.

ETA 2010-01-25: The Herald on Sunday published the story "Bonus Bonds : odds against a pot of gold" (thanks to the jouranlist for emailing the URL); they used some quotes from my interview, but not the photos taken in a bit of a rush last Thursday.